Protecting Your Nest Egg: Managing Sequencing Risk in Retirement

When constructing portfolios for our clients, we typically look to include a capital stable allocation around 2 years prior to retirement, and then for at least the first 10 years of retirement. This might be a term deposit or a conservative fund option.

The role of this component within the portfolio is to protect against sequencing risk. We know that long term stock markets will deliver us a return of 8% to 10%, however from one year to the next there is a high degree of variability. The order in which you get your returns can have a very large impact on the longevity of your savings around the point of retirement.

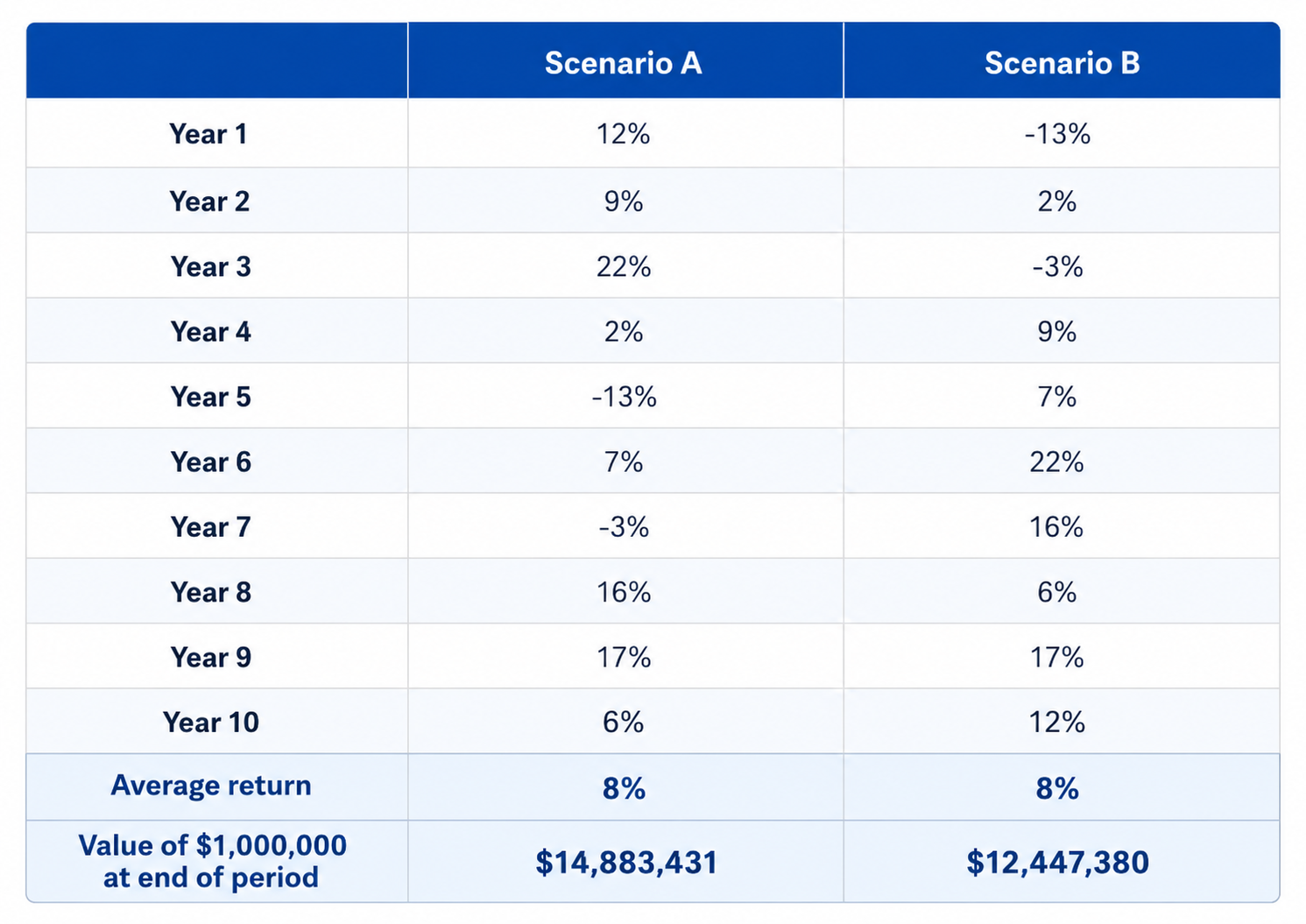

To illustrate, here’s two sequences of returns, each with the same average:

The individual yearly returns are identical in both scenarios, leading to the same average, I’ve just adjusted the order that those returns fall, with scenario B having more of the poor returns at the beginning and the better returns at the end.

As you can see, this has an impact of over $2.4million over just 10 years.

So the order your returns occur matters (a lot!), and this is even more important at the point of retirement because you will begin drawing money out, which necessitates selling assets. Your total savings are typically at their highest point too, so a 10% fall in value is a much larger dollar amount than a similar 10% fall when you are 85 and will have used up a lot of your savings. Plus your time frame isn’t 10 years as per the example, but more like 30.

The role of the capital stable portion of your portfolio is to provide a source of funding your pension drawings were it the case that the stock market had a drop in the first few years of your retirement. You could live off the capital stable money and not be forced to sell any shares, giving them time to recover. This enhances how long your savings will last, and the value of the estate that you leave behind.

If you need help with your retirement planning, that’s exactly what we do at Guidance Financial Services. Learn more below.